Every day, thousands of side-hustlers, freelancers, and independent contractors make the exact same financial mistake. They launch a photography business, start driving for a rideshare app, or open a digital marketing consultancy, and they immediately begin paying for their business expenses using their personal debit or credit cards.

When asked why they haven’t separated their finances with a dedicated business credit card, the answer is almost always identical: “I don’t have a real business yet. I don’t have an LLC, and I don’t have an EIN.”

This is one of the most pervasive and expensive myths in the world of personal finance.

You do not need an Employer Identification Number (EIN) to get a business credit card. You do not need to file complex incorporation paperwork to form a Limited Liability Company (LLC). You do not need a storefront, a payroll system, or a team of employees.

If you are mowing lawns for profit, selling vintage clothes online, or doing freelance coding from your kitchen table, the financial system already recognizes you as a legitimate business entity. You are a sole proprietor. And as a sole proprietor, you have the absolute legal right to apply for, and receive, the most lucrative business credit cards on the market using nothing but your own name and your Social Security Number (SSN).

This comprehensive guide will demystify the underwriting process for independent workers. We will walk you through exactly how to fill out a business credit card application without an EIN, explain why you desperately need to stop using your personal cards for overhead, and reveal the best financial tools designed specifically for the modern sole proprietor.

The Big Myth: Understanding the Sole Proprietorship

Before we dive into the mechanics of the application, we must dismantle the imposter syndrome that holds many freelancers back.

Many independent workers believe that a “business” must be a registered corporation. In the eyes of the law and the Internal Revenue Service (IRS), this is entirely false. A business is simply any activity you engage in with the intent to make a profit.

When you start selling your services or products without formally registering a corporate entity (like an LLC or an S-Corp), the government automatically classifies you as a Sole Proprietor.

You and the Business Are One

In a sole proprietorship, there is no legal distinction between the owner and the business. You are the business. Because you are the business, you do not need a separate tax identification number (like an EIN) to file your taxes or open financial accounts.

Your Social Security Number acts as your business’s identification number. When tax season arrives, you simply report your business income and expenses on a Schedule C form attached to your standard personal tax return.

Credit card issuers—like Chase, American Express, and Capital One—understand this intimately. They have designed their application portals to seamlessly accept applications from sole proprietors using an SSN instead of an EIN. They are hungry for your business, and they have removed the red tape to get it.

Why You Desperately Need a Business Credit Card

If you are currently paying for your web hosting, your professional software, or your business inventory with a personal credit card, you might wonder why you should bother applying for a new card at all.

Transitioning your overhead to a dedicated business credit card provides three massive, structural advantages that protect your personal life and boost your profit margins.

1. The Tax Season Shield

When you mix personal and business expenses on a single credit card, you create an accounting nightmare. Finding your deductible business expenses means combing through twelve months of statements, trying to remember if a $45 Amazon charge was for office printer ink or a birthday present for your nephew.

This co-mingling leads to missed tax deductions, which means you pay more income tax than you legally owe. By dedicating a single business credit card solely to your gig work, your credit card statement essentially becomes an automated, IRS-ready ledger. When April arrives, you simply hand the statement to your accountant or input the final numbers into your tax software.

2. Protecting Your Personal Credit Score

Your personal FICO credit score is heavily influenced by your “credit utilization ratio.” This is the percentage of your available credit that you are currently using. If you use a high percentage of your available credit, your score will plummet.

If you use a personal credit card to buy $3,000 worth of inventory for your online store, your personal credit utilization spikes, dragging down your personal credit score. This can make it difficult for you to buy a house, finance a car, or rent an apartment.

Business credit cards (with the exception of some Capital One and Discover cards) do not report your daily balances to the consumer credit bureaus. You can safely carry a high balance for a month to float a large business purchase, and your personal credit score will remain completely untouched.

3. Massive Welcome Bonuses and Multipliers

Banks desperately want the spending volume that businesses provide. To attract that volume, they offer sign-up bonuses on business cards that dwarf those offered on personal cards.

It is common to see a business credit card offer $750 or even $1,000 in cash back after meeting a minimum spending requirement. Furthermore, business cards offer elevated cash-back multipliers in categories that actually matter to a freelancer, such as advertising spend, shipping, cell phone bills, and office supplies.

The Underwriting Secret: How Banks Evaluate Sole Proprietors

A common fear among new freelancers is that they won’t be approved for a business card because their side hustle doesn’t make enough money yet.

“I only made $2,000 from my photography business last year. Why would a bank give me a $10,000 credit limit?”

To conquer this fear, you must understand how banks underwrite sole proprietors. Because you and your business are the same legal entity, the bank does not underwrite the credit card based solely on the revenue of the business. They underwrite the card based on you as a human being.

The bank will look at two primary factors:

- Your Personal Credit Score: They will pull a hard inquiry on your personal credit report (via your SSN). If you have a history of paying your personal credit cards and car loans on time, the bank trusts you.

- Your Total Personal Income: The bank will ask for your total gross annual income. This includes the money your side hustle makes, but it also includes the income from your full-time W-2 job, your spouse’s income (if you have reasonable access to it), and any other stable income streams.

If you have a 740 personal credit score and a reliable full-time job, the bank is highly likely to approve your business credit card application, even if your actual side-hustle revenue is currently very small. They know that if the business fails, you have the personal income to pay back the debt.

Step-by-Step: Filling Out the Application Without an EIN

Applying for a business credit card online takes about five minutes. However, because the forms are designed to accommodate massive corporations as well as gig workers, the terminology can feel intimidating.

Here is exactly how to fill out each section of a typical business credit card application as a sole proprietor using your SSN.

Step 1: Legal Name of Business

This is where most freelancers panic. If you do not have a registered DBA (Doing Business As) or a fictitious name filed with your state, your legal business name is simply your own full name.

If your name is Sarah Jenkins, and you run a freelance writing business, you type “Sarah Jenkins” into the Legal Business Name field. Do not make up a name like “Sarah’s Word Studio” if you have not legally registered it, as this can trigger a fraud alert and delay your application.

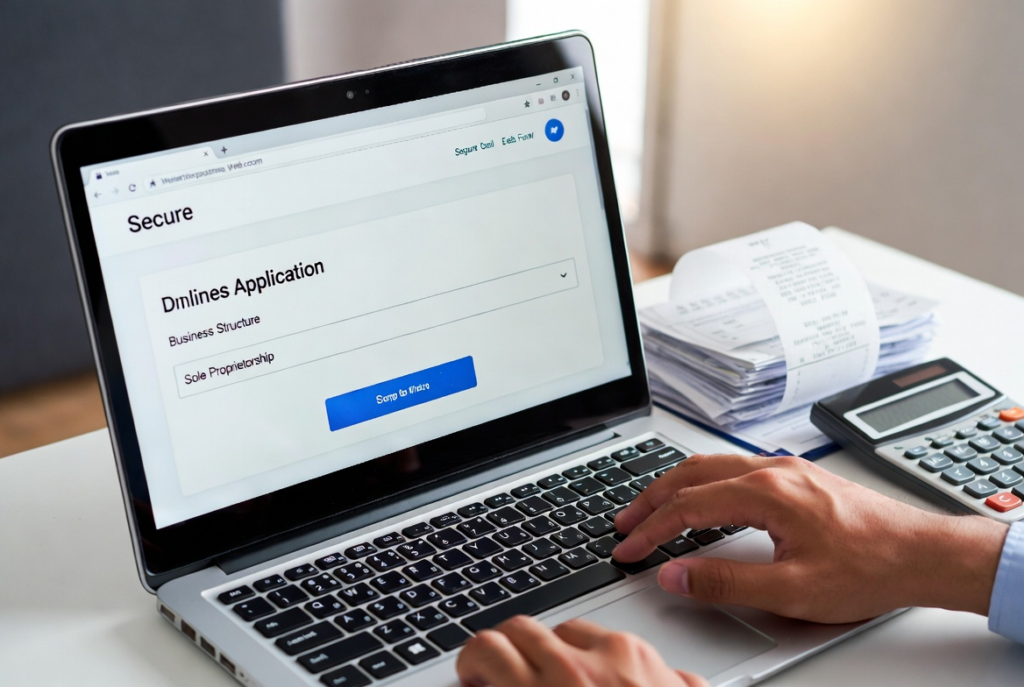

Step 2: Business Structure / Company Type

There will be a drop-down menu asking for your corporate structure (e.g., LLC, S-Corp, Partnership). You must select “Sole Proprietor” or “Sole Proprietorship.”

Step 3: Tax Identification Number (TIN / EIN)

Because you selected Sole Proprietor in the previous step, the application form will usually dynamically update. The box that asked for an EIN will now allow you to input a Social Security Number.

Simply enter your personal 9-digit SSN. This is the legal tax ID for your business.

Step 4: Business Address and Phone Number

If you work from home, drive for Uber, or operate a mobile business, your business address is simply your home residential address. Use your personal cell phone number as the business phone number.

Step 5: Industry / Business Category

The bank needs a general idea of what you do for a living. They will usually provide a dropdown menu of NAICS (North American Industry Classification System) codes or broad categories.

Choose the category that most closely matches your work. If you are a rideshare driver, look for “Transportation.” If you are an Etsy seller, look for “Retail” or “E-commerce.” Do not overthink this; it is mostly for the bank’s internal demographic data.

Step 6: Years in Business

Banks ask how long your business has been operating. Be honest. If you literally just decided to start consulting yesterday, put “0 years” or “less than 1 year.”

While a longer history is better, banks routinely approve brand-new sole proprietors based on the strength of their personal credit scores. Do not inflate this number.

Step 7: Annual Business Revenue

This asks for the gross amount of money your business brings in before expenses.

If your business is brand new, you can legitimately put “0” or provide a very conservative projection of what you expect to make in the next 12 months.

If you have been operating for a while, put your actual gross revenue from the previous year. Again, remember that the bank is primarily relying on your personal income to approve you, so a low business revenue will not necessarily result in a denial.

Step 8: Total Gross Annual Income

This is the most critical box for a sole proprietor. This is not your business revenue. This is all the money you make as a human being.

Include your salary from your day job. Include your partner’s income if you share finances and pay bills together. Include rental income and investment returns. This number proves to the bank that you have the financial stability to handle a new credit line.

Step 9: Authorizing Officer Information

Because you are the owner, you are the authorizing officer. You will fill out your personal name, your personal home address (which will likely be the same as the business address), and your SSN again to authorize the bank to pull your personal credit report.

Top Credit Cards for Sole Proprietors in 2026

Now that you know how to navigate the application, you need to choose the right tool. As an independent worker, your priorities should be avoiding annual fees, securing a strong welcome bonus, and earning high rewards on the things you actually buy.

Here are the top business credit cards designed perfectly for the sole proprietor lifestyle.

1. The Best for Pure Simplicity: The Blue Business® Plus Credit Card from American Express

If you wear multiple hats and your expenses vary wildly from day to day, tracking complex reward categories is a massive waste of time. American Express offers the ultimate “set it and forget it” solution.

- Annual Fee: $0

- The Rewards: You earn a flat 2X Membership Rewards® points on all everyday business purchases, regardless of what you are buying.

- The Limit: The 2X rate applies to the first $50,000 in purchases per calendar year, dropping to 1X thereafter (which is more than enough headroom for most side-hustlers).

Why it’s perfect for sole props: Whether you are buying a $2,000 camera lens, paying for Facebook ads, or taking a client out to lunch, you are guaranteed a strong return. The points are incredibly valuable if transferred to airline partners for personal vacations.

2. The Best for Overhead Cash Back: Chase Ink Business Cash® Credit Card

If your business has specific, recurring overhead costs—like internet, cell phone bills, and office supplies—the Chase Ink Cash card is a relentless cash-generating machine.

- Annual Fee: $0

- The Rewards: You earn a massive 5% cash back on the first $25,000 spent in combined purchases at office supply stores and on internet, cable, and phone services each account anniversary year. You also earn 2% cash back on the first $25,000 spent at gas stations and restaurants.

Why it’s perfect for sole props: Every freelancer has an internet bill and a cell phone bill. Putting those mandatory expenses on this card acts as an instant 5% discount. Furthermore, Chase is famous for offering historically massive sign-up bonuses on the Ink series, providing a massive injection of cash right when your small business needs it most.

3. The Best for High Volume Spenders: Capital One Spark Cash Select

If you have a slightly higher overhead—perhaps you are a dropshipper buying inventory, or a contractor buying raw materials—and you prefer straight cash back over travel points, Capital One offers a highly competitive tool.

- Annual Fee: $0

- The Rewards: You earn an unlimited flat 1.5% cash back on every single purchase, with absolutely no spending caps or categories to track.

Why it’s perfect for sole props: It provides a reliable, steady stream of cash back that can be redeemed in any amount at any time to directly offset your business costs. Note: Capital One does report business card activity to personal credit bureaus, so it is vital that you pay this balance in full every month to protect your personal utilization ratio.

Comparison Table: Choosing Your Business Partner

| Feature | Amex Blue Business Plus | Chase Ink Business Cash | Capital One Spark Cash Select |

| Annual Fee | $0 | $0 | $0 |

| Reward Structure | 2X Points (up to $50k/year) | 5% / 2% / 1% Tiered Cash Back | 1.5% Unlimited Cash Back |

| Best Earning Category | Flat rate on everything | Office Supplies, Internet, Telecom | Flat rate on everything |

| Reports to Personal Credit? | No (Unless you default) | No (Unless you default) | Yes |

| Ideal Sole Proprietor | The flexible traveler | The low-overhead remote worker | The high-volume buyer |

Case Study: The Wedding Photographer’s Financial Pivot

To illustrate how powerful this simple shift can be, consider the case of David, a high school teacher who shoots weddings on the weekends.

For his first two years, David operated entirely out of his personal checking account. He used his personal debit card to pay for his website hosting ($200/year), his editing software subscriptions ($600/year), and occasional lens rentals ($1,200/year).

When he booked three weddings in one month, he needed to upgrade his primary camera body, which cost $3,500. He put it on his personal credit card. His personal credit utilization spiked to 45%, and his credit score dropped by 30 points right as he and his wife were applying for a mortgage refinancing. Tax season was also a nightmare, taking him days to separate his camera rentals from his grocery bills.

The Pivot:

David finally realized he was a sole proprietor. He applied for the Amex Blue Business Plus using his SSN and his teaching salary as his primary income. He was instantly approved with a $10,000 limit.

- The Relief: He moved the $3,500 camera purchase to the new business card. His personal utilization dropped back to near zero, and his personal credit score rebounded immediately.

- The Rewards: By routing all his software, travel, and rental expenses through the business card, he generated thousands of Membership Rewards points, which he eventually used to book flights for an anniversary trip.

- The Organization: At the end of the year, he downloaded a single PDF statement from American Express. It contained every single business expense he had made for 12 months, neatly categorized. Tax season took him exactly forty-five minutes.

David didn’t change his business. He didn’t incorporate. He didn’t file paperwork with the state. He simply utilized the correct financial tool for the job.

Crucial Mistakes to Avoid as a Sole Proprietor

Having a business credit card is a powerful asset, but it comes with a strict set of rules. As a sole proprietor, your personal finances are inextricably linked to your business failure or success. You must avoid these three catastrophic errors.

1. The Co-Mingling Relapse

Once you have the business card, you must treat it as sacred. Never, under any circumstances, use the business credit card to pay for personal expenses. Do not put a personal dinner, a personal Netflix subscription, or your home mortgage on this card.

If the IRS audits your Schedule C tax return and finds personal expenses mixed in with your business ledger, they can disqualify your legitimate deductions and penalize you heavily. Keep the wall between business and personal utterly impenetrable.

2. Carrying a Balance

Business credit cards generally have higher interest rates (APRs) than personal cards. The rewards and cash back you earn are only profitable if you never pay a dime in interest.

If you use the card to float a business expense and fail to pay the statement balance in full, the 24% interest charge will instantly eradicate any 2% cash back you earned. Treat the business credit card like a debit card; only swipe it if the cash to cover the expense is already sitting in your bank account.

3. Faking Business Revenue

When applying for the card, the temptation to inflate your business revenue to “look better” to the bank is strong. Do not do this.

Banks occasionally trigger financial reviews where they ask for tax returns to verify the numbers you provided. If they discover you lied about your business revenue, they will instantly shut down all your accounts with that institution and potentially blacklist you. Be honest about your revenue; remember, they are relying primarily on your personal W-2 income to approve you anyway.

Summary

The narrative that you need an EIN, an LLC, and a team of lawyers to access commercial financial tools is a myth that actively harms independent workers. The financial system is built to support the gig economy, provided you know how to navigate it.

To recap the blueprint for success:

- Acknowledge Your Status: If you sell a product or service for profit, you are legally a Sole Proprietor.

- Use Your SSN: You can apply for top-tier business credit cards using your own name as the business name and your Social Security Number as the tax ID.

- Rely on Personal Income: Banks will underwrite your application based on your personal credit score and total gross income, making it easy for new side-hustlers to get approved.

- Protect the Wall: Once approved, strictly separate your personal and business expenses to streamline your taxes and protect your personal credit utilization.

- Choose the Right Tool: Opt for no-annual-fee cards that offer simple, flat-rate earning or rewards in categories that match your actual overhead.

Conclusion

Stepping into the world of independent work—whether as a full-time freelancer or a weekend side-hustler—is an act of immense bravery. You are taking control of your income, your schedule, and your future.

However, raw talent and hard work are not enough to sustain a business; you must also build a resilient financial infrastructure. A dedicated business credit card is the cornerstone of that foundation. It acts as an automated bookkeeper, a shield for your personal credit, and a silent partner that kicks profit back into your pocket on every transaction.

You do not need to wait until your business is “big enough” to legitimize it. Legitimize it today. Gather your personal financial information, choose a card that aligns with your goals, and apply with confidence as a sole proprietor. The tools are waiting for you; you simply have to reach out and take them.